You are currently viewing our boards as a guest which gives you limited access to view most discussions and access our other features. By joining our free community you will have access to post topics, communicate privately with other members (PM), respond to polls, upload content and access many other special features. Registration is fast, simple and absolutely free so please, join our community today!

The banners on the left side and below do not show for registered users!

If you have any problems with the registration process or your account login, please contact contact us.

Vancouver Off-Topic / Current EventsThe off-topic forum for Vancouver, funnies, non-auto centered discussions, WORK SAFE. While the rules are more relaxed here, there are still rules. Please refer to sticky thread in this forum.

Real estate here is such a shit show. A friend of mine got a brand new house in Houston, jn a nice area, for 350k usd. It’s only like 10 mins away from the ocean.

He’s like how do you Canadians afford it ? I’m like we don’t. Either you have millions of dollars or else you are barely scraping by and living off McDoubles.

Real estate here is such a shit show. A friend of mine got a brand new house in Houston, jn a nice area, for 350k usd. Its only like 10 mins away from the ocean.

Hes like how do you Canadians afford it ? Im like we dont. Either you have millions of dollars or else you are barely scraping by and living off McDoubles.

The crazy thing is his property tax would be similar to a house that cost 3.5 mill in Van.

Yeah that's one thing I noticed: property tax is a damn bargain in Canada.

Back in Menlo Park, my property tax rate was 5x that in Vancouver. A whole 1/3 of my housing cost was just property tax (the other 2/3 being mortgage payment).

Even Toronto property tax is 2.4x higher than Vancouver.

The other nice thing about Canada is the price of electricity. It's like 10-15c per kWh here? Whereas in California it's ~35c USD / kWh.

__________________ Geriatric Motoring Club Member #37

Quote:

Originally Posted by EvoFire

I need to be reliably within 10-15mins of a baked pork chops rice with lemon tea.

That's Texas though, little to no income taxes, low sales taxes, but high property taxes.

__________________

Quote:

Originally Posted by MG1

In Mike we Trust

Quote:

Originally Posted by westopher

LOOK AT ME IM MIKE AND I HAVE A BIG HOG AND I DRINK TEQULA AND WORK OUT AND LISTEN TO CHARLI XCX ON THE BEACH IN BERMUDA

Grow up fuckin Peter Pan and get a good nights rest.

That's Texas though, little to no income taxes, low sales taxes, but high property taxes.

You haveway higher electric rates and you have surge pricing in Texas. It can jump 6000% for short periods of time during high demands. Also the grid is not connected to the rest of America and it fails a lot. Houses are build a lot shittier in Texas. The min r value for insulation is r13. BC is min is R22 California is r20. Meaning it's going to take a lot more to heat and cool your home. If you have money you are going to want to have back up power. And lets not get into shootings.

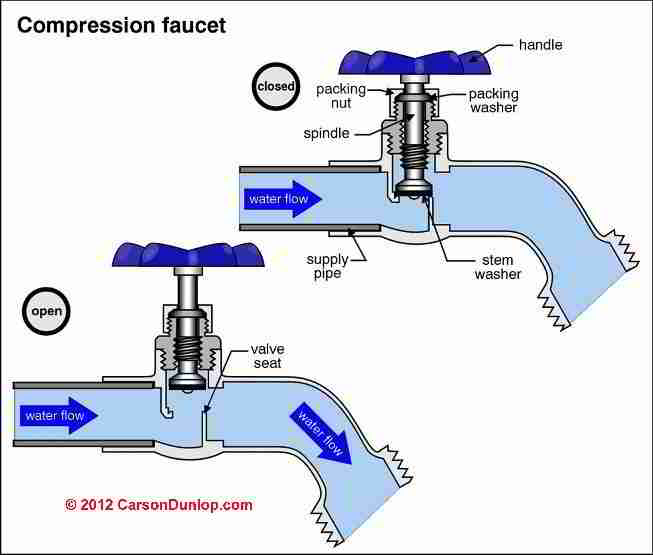

This is what happens when it goes below freezing in Texas. Pipes burst because they freeze do to poor building codes.

This is how hose bibs are set up in most places.

In Texas

In the top pic the water left in the pipe is insulated so it does not freeze. in Texas the valve shuts off the vatter right at the nob. So the water is not insulated and it freezes.

You also have electric on demand water heaters mounted on the outside. If it's cold and the power goes out they will freeze and the pipe will burst.

Those prices on those Texas homes basically mean the land is worthless. Even with Mexican slave labour it would be VERY hard to build a 2000 sq ft home for under 400-500k

So my question would be, what’s the neighborhood like and what’s the area like

I could probably sell my home and buy a low rise in Detroit, but is it worth it? Probably not

__________________

Dank memes cant melt steel beams

Add in the fact that everyone who's been on five-year fixed rate mortgages at historic rate lows and have been avoiding the financial pain all the variables have been feeling are starting to come up for renewal. This is where it's going to get even uglier. Fixed-rate holders are going to see their rates more than double and the sticker shock is going to have huge implications. In order to service mortgage debts tens of billions of dollars is about to be pulled out of the general economy to pay banks (there's a bit over 2T in mortgage debt nation-wide). So naturally home owners and renters are going to have to increase rent amounts to help their costs and on and on it goes with housing driven inflation. Canada has now bolted itself between a rock and a hard place with a highly inflated housing market and grossly excessive immigration leading to population increase and housing demand.

Friends who are realtors have told me the number of people who get accepted offers (buying or selling) and then the financing gets denied are through the roof. People can't get past the up to 9% stress test, so houses are sitting on the market longer and longer with needy buyers unable to get a mortgage. A million dollars requires the 20% deposit the average person doesn't have.

The fuse on the bomb keeps getting shorter, and Q4 2024 is when it's really going to start accelerating. 2025 and 2026 are when the bulk of the low fixed-rate mortgages turn over. Foreclosures, auto repossessions, and personal CC debts are all increasing already.

Good. Everything you are saying should lead to lower real estate prices. Are you against lower and more affordable real estate prices? Or do you want it to stay high?

__________________ Never argue with a dumbass, they drag you down to their level and try to beat you with experience

so wife wants to move. our neighborhood in coqutilam is prime for land assemblies and there's already a bunch of development starting that's going to make the area a nightmare in the coming years.

i've always liked the como lake area.

my current house is worth around the 1.5M+ but i think that might be low looking at realtor.ca. it's been nicely reno'd, new roof and hot water etc. so i think it'll be able to fetch quite a bit more. current mortgage left is maybe $150K

i want a house that will need work as I'm in construction and have the skills and contacts to build the sweat equity again and this time around design it how i want it with my connections to help with the work

say i buy a place that's $1.8M+, do you think it would be best to sell my current house and put all the money right into the new house or to keep the house, pull the equity and to rent it out.

i personally want to keep the house for a couple reasons. 1) we have somewhere to leave while i gut and reno the new one. we have a young child so i don't want her in a house getting heavily reno'd nor do i want a massively tight schedule. 2) i can rent my house for $4000 montly to help with the new mortage. 3) i want to have a house to give to my daughter as we all know price increases aren't slowing down and our kids are all screwed.

the new house will need to have a basement suite or one will be added in depending on the house. then that will help with the mortage.

thoughts?

what are the capital gains tax implications if any that i maybe need to consider?

If you decide to keep your current house and turn it into an investment property, you'd want to retain some sort of proof as the market value of your house at the time it changed from being your primary residence to your investment property. Since your property's value is not subjected to capital gain during the years when it is used as your primary residence, the proof of (property) value would come in useful should you eventually sell (or transfer home ownership title).

The most obivous, but not most accurate, proof of your property value is your BC assessment papers.

If you decide to keep your current house and turn it into an investment property, you'd want to retain some sort of proof as the market value of your house at the time it changed from being your primary residence to your investment property. Since your property's value is not subjected to capital gain during the years when it is used as your primary residence, the proof of (property) value would come in useful should you eventually sell (or transfer home ownership title).

The most obivous, but not most accurate, proof of your property value is your BC assessment papers.

Also, if im not mistaken, you can get a realtor to do an evaluation on your house. Ex: BC assesment is 1.4mil, realtor is 1.6mil.

That way when you "deem disposition" your sold value is 1.6 instead of automatic 1.4

Might save you thousands of dollars when tax time comes. On 200k difference thats probably 20-50k in tax for most people.

__________________

Quote:

Originally Posted by Mr.Money i hate people who sound like they smoke meth then pretend like they matter.

Originally Posted by ilovebacon

Does anyone have a pair of 25 pounds one-inch hole for sale at a reasonable price?

Originally Posted by bcuzracecarz

and thats all before seeing hes also posted bunny manure for sale.

so wife wants to move. our neighborhood in coqutilam is prime for land assemblies and there's already a bunch of development starting that's going to make the area a nightmare in the coming years.

i've always liked the como lake area.

my current house is worth around the 1.5M+ but i think that might be low looking at realtor.ca. it's been nicely reno'd, new roof and hot water etc. so i think it'll be able to fetch quite a bit more. current mortgage left is maybe $150K

i want a house that will need work as I'm in construction and have the skills and contacts to build the sweat equity again and this time around design it how i want it with my connections to help with the work

say i buy a place that's $1.8M+, do you think it would be best to sell my current house and put all the money right into the new house or to keep the house, pull the equity and to rent it out.

i personally want to keep the house for a couple reasons. 1) we have somewhere to leave while i gut and reno the new one. we have a young child so i don't want her in a house getting heavily reno'd nor do i want a massively tight schedule. 2) i can rent my house for $4000 montly to help with the new mortage. 3) i want to have a house to give to my daughter as we all know price increases aren't slowing down and our kids are all screwed.

the new house will need to have a basement suite or one will be added in depending on the house. then that will help with the mortage.

thoughts?

what are the capital gains tax implications if any that i maybe need to consider?

thanks guys

There are a couple things to consider.

If we figure your current house is worth $1.5M and your new house is going to be purchased (and we assume will appraise) for $1.8M, then the total value of both homes will be $3.3M. You'll need your existing $150k mortgage plus $1.8M for the new house, so a total loan required of $1.95M. $1.95M versus $3.3M is a loan to value of approx 60% which is totally achievable, and you can push this a bit higher, easily 65%.

However, the bigger question, is can you actually qualify to keep your house and buy the new one, without rental income while you are living in your old house and renovating your new?

Qualifying rate on a $1.95M mortgage is approx 7% right now for a fixed mortgage, though the actual rate will be lower when you buy the place. $1.95M mortgage, 7%, 30-year am = approx $13,000 monthly payment or $156,000 annually.

If you have no other debts, you will need to prove and declare approximately $350k in annual income on your and your wife's tax return to be conventionally approved on this.

If you meet this hurdle, I'd say this is a totally doable plan to keep your current place while you renovate the new one (as long as you can actually swing this payment).

The next question is once the new place is done and you move in, do you keep and rent or sell the current house? If you figure that you can only get $4,000 per month for your house or sell it and get $1.5M+, that's an EASY decision, you sell it. Receiving rent of $48k per year is the equivalent of a 3% rate of return on your $1.5M tied up. You could literally go buy GICs with 0 risk and get more like 5%, and options go up from there. But frankly there are a lot more components to consider than you can cover on one post here, and you might want to have a conversation with your advisor on this one.

-Mark

__________________ I'm old now - boring street cars and sweet race cars.

Hmm that place is actually much nicer than I expected from the exterior. Id say thats actually decent value albeit a very busy street

Oh I think totally the opposite.

The galley kitchen is cramped. Primary bedroom closet is pathetic. Waking up in the morning you get to look out the windows past the prison bars on to a busy street. Not to mention the view of the parking lot. All this for a cool $1.4M and $700/mo in strata fees. No thank you.

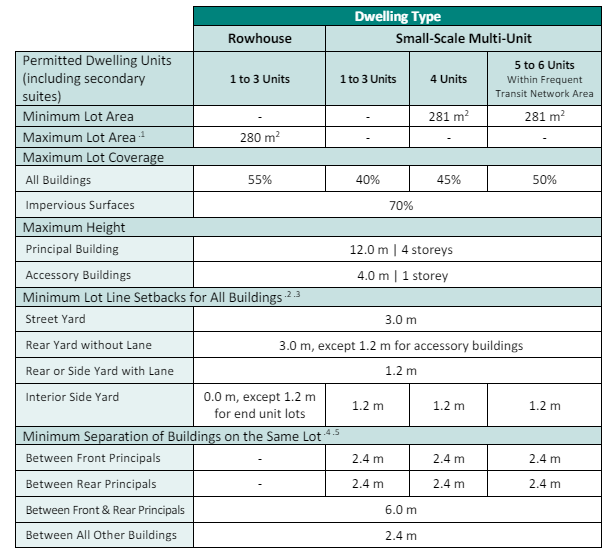

They're getting rid of all the residential zones, combining it into one overall zone and then allowing up to 6 units depending on lot size and how close it is to frequent public transit.

Our family home is on a 6600 sqft lot and we're thinking of tearing down the house and building three units if this passes. This way each sibling can have a unit and keep the land in the family.

Don't know if this applying to everywhere else in BC due to the Bill 44 thing, but first time hearing about it directly applying to my city (I lurk here and there in this thread sometimes).

EDIT: Did more digging since I was curious how big we could build, and if I'm understanding it right possibly up to four stories since they're getting rid of the floor area and gross floor area ratios.

You are currently viewing our boards as a guest which gives you limited access to view most discussions and access our other features. By joining our free community you will have access to post topics, communicate privately with other members (PM), respond to polls, upload content and access many other special features. Registration is fast, simple and absolutely free so please, join our community today!

The banners on the left side and below do not show for registered users!

You are currently viewing our boards as a guest which gives you limited access to view most discussions and access our other features. By joining our free community you will have access to post topics, communicate privately with other members (PM), respond to polls, upload content and access many other special features. Registration is fast, simple and absolutely free so please, join our community today!

The banners on the left side and below do not show for registered users!